Jets ETF Could Be Ready For Takeoff With Some Cash Finding Its Way Back Into the Market

The markets are trading as expected; a bit overbought but nothing too concerning. JETS, the ETF of global airline stocks, is still very oversold, and we see any good news on the Covid Delta variant as a catalyst to springboard this sector up quickly. It could also be worth looking at the gaming stocks which are oversold as well. Interest rates look to be rising and bond prices are falling, and the rise in bond yields should have a very positive effect on the financial and banking sectors.

There are several standard measures of the money supply, including the monetary base, M1, and M2.

Steve Meyer, one of our lead analysts, wrote this about the money supply:

•The monetary base is the sum of currency in circulation and reserve balances (deposits held by banks and other depository institutions in their accounts at the Federal Reserve).

•M1 is the sum of currency held by the public and transaction deposits at depository institutions (which are financial institutions that obtain their funds mainly through deposits from the public, such as commercial banks, savings and loan associations, savings banks, and credit unions).

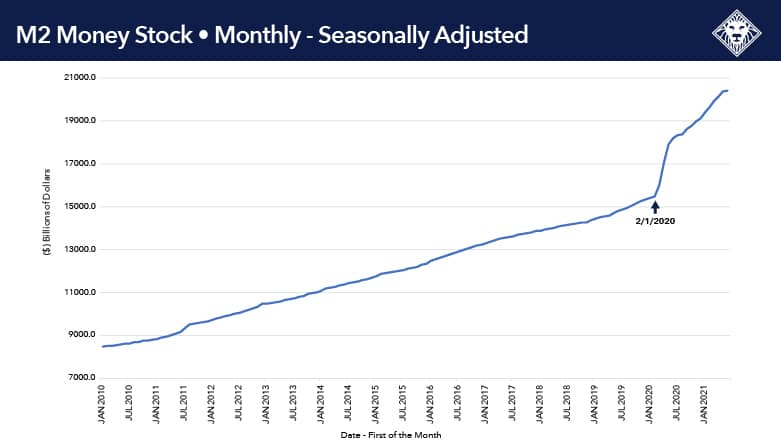

•M2 is M1 plus savings deposits, small-denomination time deposits (those issued in amounts of less than $100,000), and retail money market mutual fund shares.

Over some periods, measures of the money supply have exhibited fairly close relationships with important economic variables such as nominal gross domestic product (GDP) and the price level. Based partly on these relationships, some economists—Milton Friedman being the most famous example—have argued that the money supply provides important information about the near-term course for the economy and determines the level of prices and inflation in the long run. Central banks, including the Federal Reserve, have at times used measures of the money supply as an important guide in the conduct of monetary policy.**

Over the past few decades these relationships have been quite unstable. Nevertheless, the Federal Reserve still regularly reviews money supply data as part of a wide array of financial and economic data that policymakers review.

We have experienced an approximate 32% increase in M2 money supply compared to pre-COVID levels, leaving consumer and corporate pockets full of cash. This huge increase in money supply will drive inflation in the long term. That being said, the current U.S. monetary policy coupled with the already substantial increase in M2 money supply can easily continue to push the market to new highs.

The month over month growth in June 2021 (.09%) is the smallest monthly increase since October 2018 (.05%) compared to a 6.42% monthly increase seen in April of 2020. Are we seeing the increase in money supply begin to lose traction? Is this a decrease in inflationary pressure? Are we seeing money that has been on the sideline find its way back into the market? We can’t claim to have a crystal ball. However, like the federal reserve, we will continue to monitor this cash build up.

**federalreserve.gov